Floor Plan Financing Interest 163 J

Kbkg Tax Insight Impact Of Bonus Depreciation For Companies With Floor Plan Financing Kbkg

Instructions For Form 8990 05 2020 Internal Revenue Service

New Home Designs Perth Wa Single Storey Floor Plans More Bedroom House Plans Beautiful House Plans Modular Home Floor Plans

Https Www Houstoncpa Org Docs Librariesprovider2 Tax Expo 2020 Advanced 163j Compliance And Planning Pdf Sfvrsn D957c2b1 2

Part I The Graphic Guide To Section 163 J Tax Executive

The New Business Interest Expense Limitation Changes Squar Milner

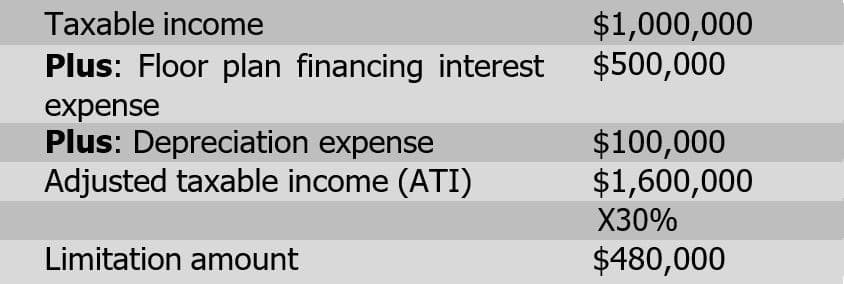

Floor plan financing interest expense is interest on debt used to finance the acquisition of motor vehicles held for sale or lease where the debt is secured by the acquired inventory.

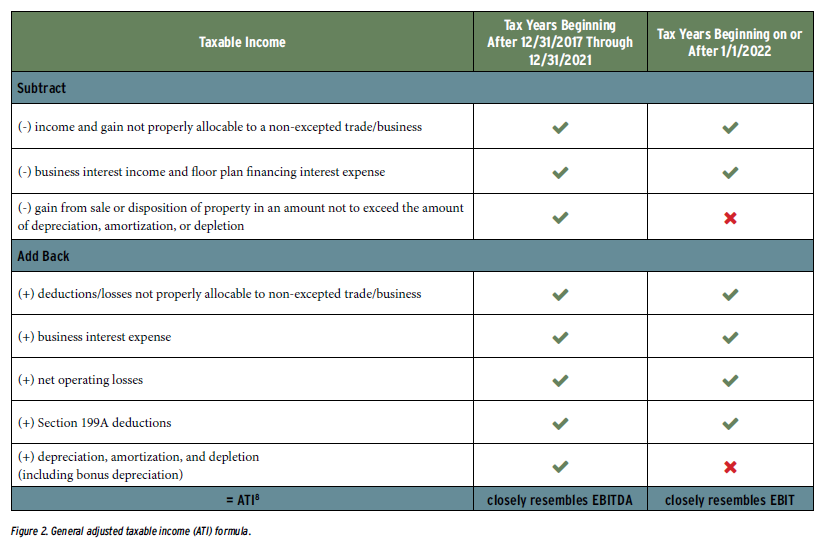

Floor plan financing interest 163 j. 163 j for tax years beginning after dec. Its floor plan financing interest for the taxable year. Floor plan financing interest expense is not subject to the section 163 j limitation. 163 j generally limits a taxpayer s business interest expense deduction to the sum of its business interest income 30 of adjusted taxable income and any floor plan financing interest expense for the tax year.

In general it limits a taxpayer s interest expense deductions for a taxable year to the sum of 30 percent of adjusted taxable income ati and its business interest income. 30 or 50 for 2019 and 2020 as amended by the cares act of the taxpayer s adjusted taxable income ati. Any business interest expense in excess of this limitation is carried forward indefinitely and may be deducted in future years. Definition of floor plan financing interest expense following the changes made to the statute discussed above the proposed regulations provide that certain business interest expense paid or accrued on indebtedness used to acquire an inventory of motor vehicles is deductible without regard to the irc 163 j limitation.

The taxpayer s floor plan financing interest expense. New section 163 j limits the taxpayer s annual deduction of interest expense to the sum of. Floor plan financing interest expense. The taxpayer s floor plan financing interest expense for the year.

Its business interest income for the taxable year. The taxpayer s business interest income. 30 of its adjusted taxable income for the taxable year. Enacted on december 22 2017 with the tax reform legislation new section 163 j 1 limits a taxpayer s annual deduction for business interest to the sum of.

Certain taxpayers involved in the sale of motor vehicles may also be able to increase their section 163 j limitation by any floor plan financing interest expense. For tax years beginning after 2017 the limitation applies to all taxpayers who have business interest expense other than certain small businesses that meet the gross receipts test in section 448 c exempt small. Tax law amended section 163 j to disallow a deduction for net business interest expense of any taxpayer in excess of 30 of a business s adjusted taxable income plus floor plan financing interest. 31 2017 business interest expense deductions are limited to the sum of.

Who is subject to the section 163 j limitation.

2019 Bonus Depreciation Update For Auto Dealers Councilor Buchanan Mitchell Cbm

Pristine Designs 163 In 2020 Lake House Plans Design House Plans

Pin On Idee Deco

The Real Estate Election Out Of The Section 163 J Business Interest Limitation Marcum Llp Accountants And Advisors

.jpg)

The Collection Honolulu Pricing Floor Plans And Video Tours

Pin On Cool Rchitechture

1930s Kitchen Diner Knock Through Google Search Kitchen Diner Reception Rooms 1930s Kitchen

Pin On Whitney

Naval Base Guam Floor Plan Flag Circle Home Q Base Housing Floor Plans Guam

Pin On Sci Fi Kitbashing Greebles

Bonus Depreciation Rules Favor Dealerships With Floor Plan Financing Interest 2019 Articles Resources Cla Cliftonlarsonallen

Pin On Let S See The Residence Halls

Final Business Interest Limitation Rules Present Opportunities 2020 Articles Resources Cla Cliftonlarsonallen